No. AI will not replace accountants. According to the U.S. Bureau of Labor Statistics, employment of accountants and auditors is projected to grow 5% from 2024 to 2034, faster than the average for all occupations. What AI is doing is automating the repetitive, rules-based tasks that have historically consumed a large portion of an accountant’s day: data entry, transaction classification, invoice matching, and preliminary reconciliation.

The profession is not shrinking. It is shifting. Accountants who lean into that shift are seeing better outcomes, handling more clients, and closing books faster. Those who ignore it are falling behind, not because AI replaced them, but because AI-enabled competitors outpaced them.

Every few months, a new headline lands: “ChatGPT passed the CPA exam.” “AI can now do your taxes.” “Accounting is one of the most automatable professions on the planet.”

If you work in accounting, run a tax firm, or are considering a career in the field, you have probably read a version of that story more than once, and each time, it carries a little more weight.

The anxiety is understandable. Accounting is a profession built on precision, process, and pattern recognition, exactly the things that modern AI systems are becoming very good at. But the question of whether AI will replace accountants is not a simple yes-or-no. It is a question that deserves a grounded, data-backed answer rather than a clickbait prediction.

And in 2026, the data is finally clear enough to give one.

This article is written for accounting firm owners, CPAs, enrolled agents, bookkeepers, and accounting students who want to understand what is actually happening to the profession, not what the most alarming headline says about it.

If you are making decisions about your career, your team, your technology stack, or your firm’s long-term strategy, this article is for you.

Table of Contents Show

What the Numbers Actually Say About Accounting Jobs and AI

Before the interpretation, it helps to look at what the labor data shows without any spin applied.

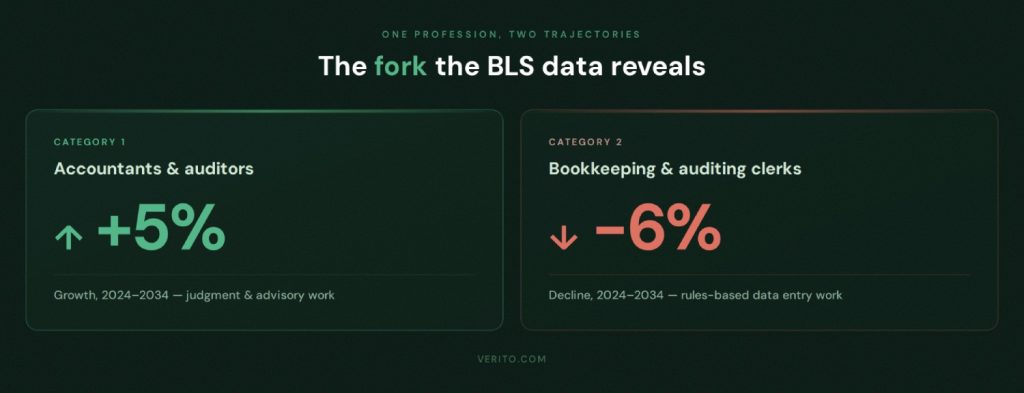

The U.S. Bureau of Labor Statistics projects that employment of accountants and auditors will grow 5% from 2024 to 2034, a rate that is faster than the average across all occupations. The BLS also projects approximately 124,200 openings for accountants and auditors each year over that same decade.

These are not the numbers of a profession under siege. They are the numbers of a profession in sustained, above-average demand.

But here is where the story gets more nuanced, and where most articles on this topic make a critical error.

The Two Categories You Need to Separate

The BLS data draws a clear line between two distinct groups, and conflating them is the source of most of the confusion in headlines about AI and accounting.

For accountants and auditors: the licensed, judgment-driven professionals who prepare complex tax returns, conduct audits, provide financial advisory, and sign off on financial statements, the outlook is growth. For bookkeeping, accounting, and auditing clerks, the category that covers high-volume, rules-based data entry and transaction recording, the Bureau of Labor Statistics projects a 6% decline in employment from 2024 to 2034.

That six percentage point gap tells the whole story. AI is automating clerical accounting work. It is not automating professional accounting judgment.

To put more texture on the labor picture: the unemployment rate for accountants and auditors was just 2.0% in 2025, according to BLS data, well below the national year-end rate of 4.4%.

Robert Half’s 2026 research found that 61% of finance and accounting hiring managers say it is much harder to find skilled professionals today than it was a year ago. The talent pipeline is tighter than the headlines suggest, and salaries are reflecting that.

Public accounting roles in tax, audit, and assurance are projected to see 3.7% salary growth year-over-year in 2026, outpacing the 2.1% average increase across all finance and accounting roles, according to Robert Half’s 2026 Salary Guide.

The professional accounting job market in 2026 is not a market in crisis. It is a market in transition.

What AI is Actually Doing in Accounting Right Now

Knowing that the profession is growing does not fully answer the question that keeps firm owners and working CPAs up at night.

That question is not really “will I be replaced?” It is “how is my day-to-day work changing, and am I keeping pace?” Those are fair questions, and the answer requires honesty about what AI is and is not currently doing inside accounting firms.

According to the 2025 Intuit QuickBooks Accountant Technology Survey, which gathered responses from 700 accounting professionals across the U.S., 46% of accountants now report using AI every day. That is not a niche early-adopter stat.It is nearly half the profession using these tools as part of their regular workflow. A separate report from Wolters Kluwer found that AI adoption in accounting firms leapt from 9% in 2024 to 41% in 2025, a jump that signals a genuine shift from experimentation to operational integration.

What is AI actually doing in accounting firms?

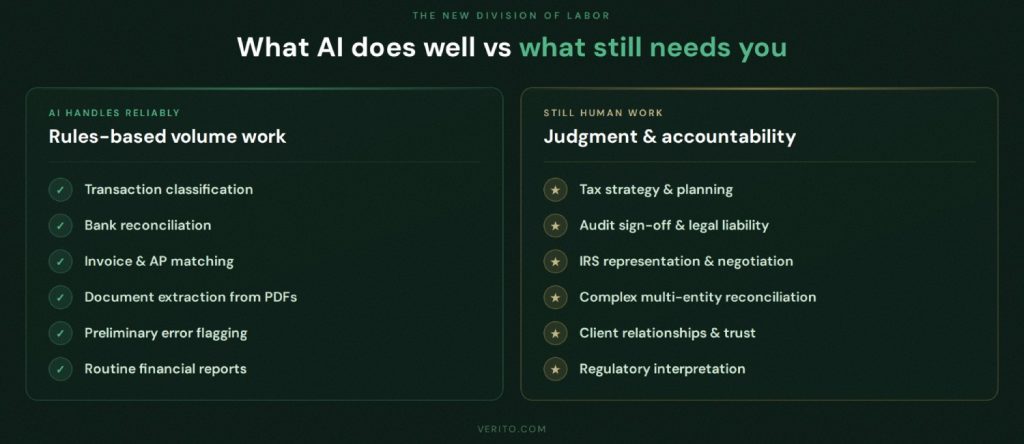

The tasks that have moved most reliably into automation are the high-volume, rules-based ones: transaction classification and categorization, bank reconciliation, invoice matching, accounts payable processing, document extraction from scanned PDFs and uploaded files, preliminary error flagging in financial statements, and the generation of routine financial reports from structured data.

Research from Stanford Graduate School of Business, studying early AI adoption across small and mid-sized accounting firms, found that accountants using AI-assisted workflows consistently supported more clients per week and spent significantly less time on routine back-office processing than those using traditional methods, with no corresponding loss in output quality.

The productivity gains are real. AI adoption among accounting firms roughly doubled between 2024 and 2025, jumping from 9% to 41% according to Wolters Kluwer’s annual technology survey, a rate of change that signals genuine operational integration rather than experimentation.

Perhaps most importantly, the shift to AI did not come at the cost of quality. According to the same survey from Intuit, 81% of accountants say AI has positively impacted their productivity, and 86% say it has reduced their mental load doing day-to-day tasks.

What AI Still Cannot Do

Understanding what AI handles well is only half the picture. The other half is just as important for anyone making decisions about their career or their firm.

Professional judgment remains stubbornly human. Tax strategy and planning require an understanding of a client’s full financial picture, their personal goals, their risk tolerance, and regulatory interpretations that are genuinely ambiguous.

Audit sign-off requires a licensed professional who accepts legal accountability for that signature. IRS representation, particularly in contentious cases, requires someone who can read a room, negotiate a position, and adapt in real time. Complex multi-entity reconciliation with exceptions, edge cases, or cross-jurisdictional considerations still requires a human who understands context.

Stanford GSB research on AI adoption in accounting firms found that senior accountants who treat AI as a collaborator, stepping in when confidence drops and applying oversight where it matters most, see significantly stronger performance gains than junior staff who accept AI-generated outputs at face value.

That finding is not a warning about AI. It is a description of how the profession is stratifying. The accountants who are thriving with AI are not those who use it least. They are those who use it most critically.

The Accounting Roles Most and Least at Risk

Given what AI can and cannot do, it is possible to map the professional landscape with reasonable clarity. Not all accounting roles carry the same exposure, and understanding where the risk concentrates is more useful than a blanket answer in either direction.

The following table summarizes where the risk of automation displacement is highest and lowest, based on BLS projections and current AI capability:

| Role Type | Risk Level | Primary Reason |

|---|---|---|

| Bookkeeping and data-entry clerks | High | Core tasks (transaction recording, reconciliation) are now automatable at scale |

| Accounts payable / receivable processors (manual) | High | Invoice matching and payment processing are heavily automated by current tools |

| Junior staff performing only transaction-level work | Medium-High | Limited exposure to judgment tasks; most value is in volume processing |

| Staff accountants with advisory involvement | Medium | Partial automation of routine tasks; judgment work insulates the role |

| CPAs with tax strategy and planning focus | Low | Requires contextual judgment, client relationship, and regulatory interpretation |

| Enrolled agents handling IRS representation | Low | Negotiation, advocacy, and legal standing require a licensed human |

| Forensic accountants and auditors | Low | Audit sign-off carries legal liability; fraud detection still requires human pattern recognition |

| Firm principals with client relationship roles | Low | Trust, relationship capital, and business development are not automatable |

The pattern here is not surprising once you see it clearly. Roles built on volume processing face real pressure from AI-driven accounting automation. Roles built on judgment, accountability, client trust, and regulatory interpretation are not only surviving, they are gaining value.

The 2025 Intuit survey found that 93% of accountants are already using AI to support strategic business advisory services, including generating financial summaries and creating real-time insights for clients. Advisory is not a future destination. It is already where the work is going.

Why the Firms Getting the Most from AI Have One Thing in Common

Here is the part of the AI-in-accounting conversation that almost no one talks about, and it is the part that has the most practical consequence for firm owners making technology decisions today.

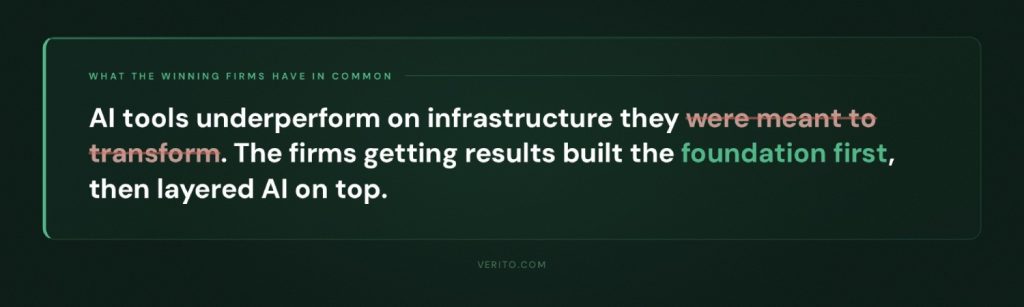

AI accounting tools, whether that means AI-assisted reconciliation software, intelligent document processing layered over Drake Tax or Lacerte, or machine learning modules built into QuickBooks workflows, run as software. And software performs only as well as the infrastructure it runs on.

Firms that have attempted to run AI-assisted workflows on aging local servers, or on shared cloud hosting where resources are split across multiple clients, consistently report the same problems. Slowdowns during peak filing season. Access failures when three or four staff members are processing simultaneously. Compliance gaps because local machines do not maintain the audit trails, encryption standards, or backup regimes required under IRS Publication 4557 and the FTC Safeguards Rule.

When an AI tool is supposed to cut reconciliation time by 75% but the server it runs on throttles under load, the efficiency gain evaporates.

The firms reporting the strongest, most consistent results from AI adoption are, with very few exceptions, firms that moved to dedicated private cloud infrastructure before adopting AI tools, not after. A dedicated cloud server means the firm’s accounting software and its AI-assisted add-ons are running on isolated, properly resourced compute, not competing with other tenants for bandwidth or processing power.

Access from anywhere is consistent. Performance during tax season, when every firm is running hot simultaneously, is predictable.

Verito’s VeritSpace product is purpose-built for this. It provides dedicated private cloud hosting for accounting and tax firms, with certified engineers who support AI tool integrations as part of the onboarding and ongoing support relationship.

VeritCertified (Verito’s internal engineer certification program) is not a marketing designation; it is a structured internal certification that covers accounting software troubleshooting, cybersecurity operations, and application-specific labs for platforms like QuickBooks, Lacerte, UltraTax, and CCH Axcess.

Firms do not have to figure out compatibility between new AI tools and their hosting environment on their own. For a deeper look at what this infrastructure layer actually involves, the guide on cloud hosting for accountants walks through the key considerations.

If you are evaluating whether your firm’s technology stack can support the AI tools you want to adopt, VeritSpace dedicated hosting plans start at $69 per user per month with a 15-day free trial and no contracts.

What Accountants Should Actually Do Differently in 2026

The data shapes a clear directive, even if it is not particularly dramatic. The accountants and firms that are positioning well for the next five years are not doing anything radical. They are making a few specific changes to how they work and what they invest in.

The first change is learning to direct AI rather than just use it. Accountants who understand which tasks their AI tools handle reliably, which outputs need human verification, and when to override a flagged result consistently outperform those who treat AI as a black box. The Stanford research was explicit on this: treating AI as a collaborator rather than an oracle is what separates performance gains from false confidence.

The second change is adjusting the service mix. Transaction processing work is increasingly commoditized by AI-driven accounting automation. Advisory work, financial planning, specialized tax strategy, and client-facing consulting are not. Firms that shift their billing model toward higher-judgment services are seeing stronger revenue per partner, and clients are paying premiums for it. The Intuit survey found that 79% of accountants expect competition for high-value advisory clients to increase in the coming year. The race to advisory is already on.

The third change is the one most firms are getting wrong: compliance documentation. Adding AI tools to a firm’s technology stack without updating the firm’s Written Information Security Plan is not a minor oversight.

Under IRS Publication 4557 and the FTC Safeguards Rule, tax and accounting firms are legally required to maintain documented information security practices that reflect their actual operating environment. A firm that adds AI-assisted document processing to its workflow has changed that environment.

The WISP needs to reflect the change. Verito’s managed IT support for accounting firms includes WISP documentation and compliance alignment as part of the VeritGuard service, which handles local devices, endpoint protection, and security monitoring alongside the cloud hosting environment.

The fourth change is infrastructure. This is not a sales point. It is a practical observation: AI tools underperform on infrastructure that was not designed to support them. Firms waiting to upgrade their technology foundation until after they adopt AI tools tend to adopt poorly and get disappointed.

Is Accounting Still a Good Career in 2026?

Yes. Unambiguously, yes.

The BLS projects 5% growth for accountants and auditors through 2034, with 124,200 openings per year. The unemployment rate for the profession sat at 2.0% in 2025, in a labor market where the national rate was 4.4%. Salaries are rising faster than the all-occupations average. The talent pipeline is failing to keep pace with demand, which is good news for anyone already in the profession or entering it with the right skills.

The caveat matters, and it is worth stating plainly. A career in accounting built primarily on bookkeeping, data entry, and transaction recording faces a more uncertain trajectory. The BLS data is clear on that. A career built on tax strategy, compliance advisory, client relationships, specialized industry expertise, or financial planning is built on ground that AI is not capable of replacing, and the demand for it is growing.

The pattern is not new. When spreadsheet software arrived in the 1980s, it eliminated a significant number of manual ledger-keeping positions. It did not eliminate accountants. It freed accountants from low-value work and raised the floor of what clients expected from them.

AI is doing the same thing at a faster pace and a larger scale. The accountants who are thriving through that transition are the ones investing in judgment, specialization, and the technology infrastructure that lets them do both efficiently. For those entering the field or repositioning within it, how you present those skills on paper matters just as much as developing them — a strong public accountant CV guide can help you frame your advisory capabilities and technical proficiencies in a way that reflects where the profession is actually heading.

The firms making that investment well are the ones worth studying. They have dedicated cloud environments, documented security practices, AI tools that are properly integrated, and advisors on call who understand both the software and the compliance landscape.

Explore the guide on the best software for accounting firms in 2026 for a structured look at how forward-thinking firms are assembling that stack.

And if your firm is ready to make the infrastructure move that supports everything else, you can future-proof your firm starting with the technology foundation.

Frequently Asked Questions

1. Will AI replace accountants?

No. The U.S. Bureau of Labor Statistics projects employment for accountants and auditors will grow 5% from 2024 to 2034, faster than the average for all occupations, with approximately 124,200 annual openings projected over the decade.

AI is automating repetitive tasks like data entry, transaction classification, and routine reconciliation. Demand for judgment-driven, advisory, and compliance work is growing, not declining. The profession is evolving, but it is not disappearing.2. What accounting tasks will AI automate?

AI is already handling transaction classification, invoice matching, bank reconciliation, document extraction from scanned files, preliminary error flagging in financial statements, and generation of routine financial reports.

These are high-volume, rules-based tasks. Work requiring professional judgment such as tax strategy, audit sign-off, IRS representation, and complex multi-entity accounting is not reliably automated by current AI systems.3. Will AI replace bookkeepers?

The risk is meaningfully higher for bookkeepers than for licensed CPAs or enrolled agents. The BLS projects a 6% decline in employment for bookkeeping, accounting, and auditing clerks from 2024 to 2034, driven largely by automation of repetitive data entry and transaction recording. Bookkeepers who expand into advisory support, software management, or client-facing financial analysis are better positioned than those whose work is concentrated in transaction recording alone.

4. What skills do accountants need to stay relevant in the age of AI?

The accountants seeing the strongest results with AI are those who treat it as a collaborator rather than an oracle. That means understanding what the tools can and cannot do, verifying outputs critically, and applying judgment where AI confidence is low. Beyond that, advisory skills, regulatory expertise, client communication, and cross-functional financial analysis are increasingly valuable because they are difficult to automate.

5. Is it worth becoming an accountant in 2026?

Yes, with a focused strategy. The BLS projects strong growth for accountants and auditors through 2034. Salaries are rising faster than the profession-wide average. The talent shortage is real and working in favor of qualified professionals. Students and career-changers entering accounting today with a focus on advisory services, specialized tax, compliance, or data-driven financial analysis are entering a profession with genuine long-term demand, not one under threat of extinction.

6. How does cloud infrastructure relate to AI tools in accounting?

AI-assisted accounting tools, from reconciliation software to document processing systems to AI-enhanced tax platforms, run as software. Their performance depends on the infrastructure beneath them. Firms running these tools on dedicated private cloud servers consistently report better performance, fewer slowdowns during peak season, and stronger compliance posture than firms on aging local machines or shared hosting environments. The infrastructure decision often determines whether AI adoption delivers its promised efficiency gains or falls short.

Closing

The fear that AI will replace accountants is grounded in a real observation: the profession is changing faster than it has in decades.

But “changing” and “disappearing” are not the same thing. The data from BLS, Stanford, Robert Half, and Intuit all point toward the same conclusion. Accountants are not becoming obsolete. They are being asked to operate at a higher level, with better tools, on better infrastructure, delivering more value per hour than they could before.

The firms that are getting this right are not the ones with the most advanced AI tools. They are the ones with the right foundation: cloud environments that support the tools, documented compliance practices that reflect the actual operating environment, and engineers who understand both the technology and the industry it serves.